A Deep Dive into the 2018 Internet Trends Report

At Code Conference every year, KPCB’s Mary Meeker delivers her Internet Trends Report — a State of the Union for the tech industry. Since software has eaten the world, the report also covers the current socio-economic trends extensively. For the best part, it comes packed with data and numbers sprinkled over 250+ slides. Here’s everything you can learn from this year’s report summed up in 12 minutes or less.

1. Mobile and Internet users growth

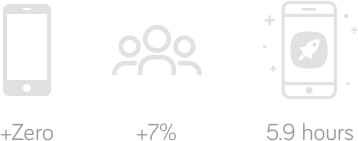

2017 saw zero growth in new smartphone shipments and only a mere 7% growth in internet users, with more than half the world population (3.6B) now connected to the internet.

When it comes to internet usage, growth remains solid with an average 5.9 hours spent on digital media usage per adult . Whether this is good or bad depends on how this time is being spent — innovation and competition are driving product improvements leading to more useful apps.

2. Innovation and Competition

Our mobile Devices are becoming better, faster and cheaper. Access has only become easier with an exploding number of Wifi networks. An increased focus on better UX/UI Design has dramatically increased Simplicity of the apps. When it comes to Payments, the digital reach is expanding, with declining friction and emergence of digital currencies (cryptos). When it comes to Local, offline connections are being driven by online network effects (Nextdoor.) Extensibility of Messaging is expanding with bots. Mobile Video adoption is climbing, with new content types expanding rapidly (Twitch.) Voice has seen a technology lift off with Google’s voice recognition accuracy now better than the human baseline of 95%. Amazon Echo and Echo Skills have seen a product lift-off too!

Aggressive competition is driving investment in Research & Development (R&D) and increasing Capital Expenditures (CapEx), which in turn are driving Innovation and Growth. In the USA, 6 of top 15 “R&D+CapEx” investors are tech companies and the tech sector is the largest and the fastest growing here.

3. Personalization and Scrutiny

Personalization presents a Privacy Paradox: while data improves engagement and experiences driving growth, it also drives scrutiny from regulators. This includes **Privacy (**GDPR), Competition (Google Shopping fined in EU), Safety/Content: (Germany Network Enforcement Act) and Taxes (EU found Luxembourg gave illegal tax benefits to Amazon).

Product designers have to keep in mind that there are unintended consequences of products that connect us en masse. Regulators have to remember that there are unintended consequences of regulation, most importantly, that of stifling innovation.

4. E-Commerce

E-Commerce acceleration continues with a growth rate of +16% vs. +14% Y/Y (Year-over-Year) for the USA. E-commerce is now 13% of total retail sales. Amazon’s E-Commerce Share Gains continued at 28% vs. 20% in 2013.

Whether you are an offline store or not, it’s easy to start an e-commerce retail shop today: Set up a Point-of-sale Payment System (Square), set up an Online Store (Shopify), integrate Online Payment (Stripe), integrate Fraud Prevention (Signifyd) and Purchase Financing (Affirm), have good Customer Support (Intercom), Find Customers (Criteo) and finally, Deliver the product (UPS+FedEx+USPS).

Product Finding

Online Product Finding is going through an evolution, now being done primarily via search and social discovery.

Search leads the way with 49% of product searches starting at Amazon and 36% at other Search Engines (primarily Google.) Google has gone from being just an Advertiser to a Retailer with Google Home ordering stuff for you. Amazon, on the other hand, has gone from being just a Retailer to an Advertiser, with Sponsored Results in searches.

Social Discovery, i.e., Facebook/Instagram, is emerging and is getting more Data-Driven, Personalized and Competitive making the whole process more efficient. Facebook E-Commerce CTRs are rising, but eCPM is outpacing it leading to reduced ROIs over the years. LTV/CAC is an increasingly important metric for retailers/brands. So much so that Facebook’s own Ad Analytics Tools for Advertisers now come with LTV Integration. Facebook’s annualized revenue per daily user is $34 (Q1 2018), rising from $16 in Q1 2015.

Between the 1890s to 2010s, Commerce Drivers evolved from Demographic to Brand to Utility to now finally Data.

Product Purchases are evolving from Buying to Subscribing. Subscription Growth is being driven by Access, Selection, Price, User Experience, and Personalization. Free to Paid Conversion seems driven, in large part, by the User Experience (Spotify.)

Shopping+Entertainment is a highly potent combination: Mobile Shopping Usage has seen 54% Session Growth vs. average 6% Growth for other Session types. Product and Price Discovery is now often Video-Enabled (YouTube ads, Taobao), often Social and Gamified (Wish with Hourly Deals, Pinduoduo with Friend Referrals reducing prices)

Physical Retail is seeing Long-Term Growth Deceleration, but China’s “New Retail” (discussed in China section later) is very interesting. While Alibaba has Higher Gross Merchandise Volume (GMV), Amazon has Higher Revenue. Internet Retail Advertising is seeing growth continue with the shift to mobile @ 22% Y/Y, but Accountability is rising — P&G Cut $140M in Digital Ad Spending, Unilever Threatened to cut budgets. Google, YouTube and Facebook have to respond by pushing for Content Initiatives.

5. Consumer Spending

Household Debt is now at highest level ever and rising.

Personal Saving Rate has fallen to 3% vs. 12% 50 years ago.

Debt-to-Annual-Income Ratio is rising with the value now at 22%.

If you look at Relative Household Spending, the share of Shelter, Pensions/Insurance, and Healthcare is rising over time.

- Shelter: US cities are less densely populated and US homes are bigger vs. the developed world. Besides, Residents per household fell to 2.5 form 3 in 1972. Airbnb increases the utility of space to contain spending on Shelter.

- Healthcare: Healthcare has been the fastest relative % grower due to increasing shift to consumers @ 18% vs 14% (1999). Deductible costs are rising with Employees @ $2K+ Deductible now at 22% vs. 7% in 2009.

This has led to Increasing Consumer Expectations and consumerization of health care: Modern Retail Experience (OneMedical), Digital Healthcare Management (Oscar), On-Demand Access (Capsule), Vertical Expertise (Women’s Healthcare Specific Solutions: Nurx), Transparent Pricing (Dr. Consulta) and Simple Payments (Cedar) are all great sub-verticals and examples of consumerization of healthcare.

The Relative Household Spending share of Food, Entertainment, and Apparel are falling over time:

- Grocery Competition has led to declining Grocery Price Growth. E-Commerce is helping reduce prices for consumers: Consumer Good Prices have fallen -3% online vs. -1% offline over last 2.25 years.

- The cost of Transport is flat, but it’s the #3 segment just behind Shelter and Taxes. Uber increases the utility of vehicles and reduces relative spend on them. Uber also has lower commute cost vs. personal car in 4 of 5 largest US cities (NYC, Chicago, DC and LA.)

6. Tech Disruption and the Job Market.

Tech Disruption is not new, but it’s accelerating. If you look at New Tech Adoption Curves, the time taken for 25% penetration for new technologies has been falling over the past century. Today’s Tech Disruption Drivers are Rising & Cheaper Compute Power & Storage Capacity, Rising & Cheaper Connectivity and Data Sharing.

New Technologies have created and displaced jobs historically — aircraft jobs replaced locomotive jobs, services jobs replaced agriculture jobs, and so on. The last 70 years have seen the GDP rise, but unemployment has stayed between 2.9% to 9.7%. Today, the Job Market looks solid with 3.9% Unemployment rate vs. 5.8% 70-year average and the Consumer Confidence at 125 vs. 87 for 55-year average. Furthermore, Job openings are at a 17-year high at 7MM, about 3x as high as the 2009 trough.

The Job Expectations are Evolving. Most Desired Non-Monetary Benefit now is to be able to work from home (with 35% of respondents noting it as a factor that will persuade them to switch from their current job) & flexible work hours (51%). Technology makes freelance work easier to find — freelance workforce has seen 3x faster growth vs. total workforce.

We’re seeing On-Demand Jobs at big numbers with high growth. They fill needs for workers who want extra income or flexibility, or have underutilized skills/assets. Few examples:

- Uber now has 3MM Global Driver-Partners with ~50% Y/Y growth. Top motivations to drive are: “Set Own Hours”, “Work/Life Balance” and “Maintain Steady Income.”

- Etsy now has 2MM Global Active Sellers. One interesting motivation to sell on Etsy is that “Creativity Provides Happiness” (which, by all means, is very real!)

- Airbnb has 5MM Global Active Listings, with top motivation being to “Use the Earnings to Stay in the Home”.

Take a deep breath. You’re half-way through :)

7. Data Gathering + Sharing + Optimization

Data has been being gathered for years, starting with Mainframe adoption in governments and businesses all the way back since the 1970s to consumer mobiles (iPhone) and the cloud (AWS) in 2000s. It’s enabled by Consumer Mobile Adoption, Social Media Adoption, and Sensor Pervasiveness.

Data is an Important Driver of Customer Satisfaction (Amazon, Google with more personalized “Near me” results, Netflix/Spotify with better recommendations and playlists, Priceline/Booking.com)

Data improves Predictive Ability of Many Services, and Data volume is foundational to algorithm refinement and AI Performance.

AI Service Platforms for Others are Emerging from Internet Leaders:

- Amazon AWS AI Services/Infrastructure. Examples here include the Rekognition Image Recognition, Scalable GPU Compute Clusters, SageMaker ML Framework and the Comprehend Language Processing.

- Google Cloud AI Services / Infrastructure: GC Vision API, Tensor Processing Units (TPUs), Cloud AutoML — Custom Models and Dialogflow Conversational Platform are all great products here.

Data Sharing creates Multi-Faceted Challenges. Data and Consumers have a Love/Hate Relationship. US consumers share data for “clear personal benefit” or with friends & family. They protect data when benefits are not clear. Hence, it’s in the interest of internet companies to make consumer privacy tools more accessible.

China is encouraging Data Collection (more on this in the China section). Cybersecurity Threats are becoming increasingly sophisticated, and they’re targeting data.

8. Global Internet Leadership & Artificial Intelligence

If you looked at today’s top 20 Worldwide Internet Leaders 5 Years ago: 9 were US companies, and two were Chinese. Today, those numbers are 11 US and 9 Chinese. Also, China is now the #1 Worldwide OEM for Smartphones with 40% share vs. 0% just ten years ago. In the meantime, USA went from 3% to 15%.

USA & China are emerging to be the two AI superpowers. China’s momentum is strong with rapidly rising student graduation rates and the government highly focused on developing AI. Also, China has feature and data-rich Internet Platforms, the largest number of users in one country, who are more willing to share data for benefits. All these are providing fuel for rapid AI Advancements.

The USA is ahead for now, but China is focussed, organized and gaining. Eric Schmidt guesses about ~five years to parity between the two countries.

9. Economic Growth Drivers

Economic Growth Drivers evolve. Today, Compute Power & Human Potential are the biggest ones. The latter brings us to the importance of Lifelong Learning. It’s crucial in the evolving work environment of today with tools getting better and more accessible. For some stats, Coursera reported having 33MM Learners (up +30%) and YouTube’s Educational content usage is ramping fast too. More than 50% freelancers updated their skills within past six months. On the enterprise side, employee re-training engagement is high (Pluralsight).

10. China

Two significant trends have emerged in China over the past few years: Robust Entertainment and Retail Innovation. Before we get into them, it’s good to note that macro trends continue to stay healthy in China: Consumer Confidence is near a 4-year high, Manufacturing Index is expanding, and GDP Growth increasingly was driven by Domestic Consumption (62% vs. 35%). As for Internet Usage, China now has 753MM Internet Users, with data usage growth by +162% for the year (vs. +124% for the year before).

A. Robust Entertainment

Short form video is proliferating with 100MM+ Daily Active Users (DAUs) and High Engagement (50-minute daily average) for apps like Douyin (aka Tik-Tok, a music video platform and social network) and Kauishou (video sharing platform.)

Long form video content budgets exceeded TV Networks’ budgets for the first time last year.

Team-based multi-player mobile games like Honor of Kings (80MM+ DAU) and PUBG Mobile (50MM+ DAU) are growing fast.

B. Retail Innovation

China’s E-Commerce share gains continued with highest Penetration Rate @ 20% of Retail Sales (and is fastest growing.) Mobile E-Commerce is at 73% of Gross Merchandise Volume (GMV), with GMV growth itself strong at 28% Y/Y.

Retail Innovation in China Spreading from Online to Offline. Two example worthy of note:

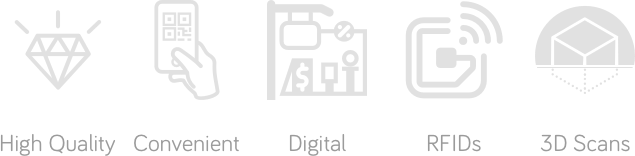

- Hema Stores are High Quality (cook-to-order chefs), Convenient (selection based on customer data and have AliPay integration) and Digital (real-time e-commerce with a ceiling-conveyor system for in-store fulfillment with 30-minute delivery.)

- Belle is a women’s shoe retailer re-imagining the offline retail experience with Online Analytics (In-store traffic heat maps, RFID in shoes/floor-mat for conversion analysis) and 3D Foot Scans for personalization.

Online Payments, Advertising, and On-Demand Transportation are all growing rapidly too.

11. Enterprise Software and Messaging Threads

Consumer-like enterprise apps like Slack and Dropbox have changed enterprise computing for the better. It’s interesting to note that Dropbox and Slack have had slightly different storylines. Dropbox has always been consumer grade with an enterprise appeal. Slack has always been enterprise grade with a consumer appeal.

Messaging Threads are transforming communication and collaboration.

Across enterprises, they are leading to distributed and increased productivity. Slack, Dropbox Paper, Zoom and Intercom are all great examples of organizing information and teams and providing context and history. While Google set out to organize the world’s information and make it more accessible and useful, these enterprise apps are trying to do the same within the companies.

On the consumer side, messaging threads are becoming more central to the interface — from Snapchat to Square Cash to even Strava.

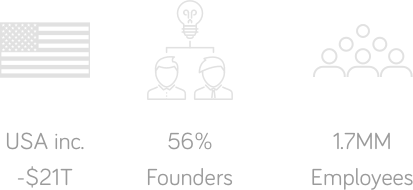

12. USA Inc. and Immigration

USA Inc. is the company where your tax dollars go. It has had net losses in the past 45 out of 50 years, is severely in debt, and has had a -19% Average Net Margin over past 30 years. Our growing debt commitments are a non-trivial challenge. Debt/GDP Ratio is now the highest level since World War II. The principal debt drivers are the Medicare & Medicaid Entitlements.

Immigration: 56% of most highly valued tech companies were founded by 1st or 2nd generation Americans. They have 1.7MM employees. Being an immigrant founder myself, I can personally attest that the “USA immigration experience” is not a very pleasant one, and we need to fix it.

Again, huge thanks to Mary Meeker and her colleagues at KPCB and collaborators for the original report. You can find all the slides here. This should be a required reading for anyone in the tech space, not just to know what’s going on, but to understand what matters.

Hi! I’m Anant and I’m one of the co-founders of Commonlounge, an educational platform with wiki-based short courses. I also write weekly book reviews on my blog and talk to people on Twitter. Come say hi 👋